We’d recently written a piece on the importance of following the Treasury’s projected Treasury General Account Balance (TGA). On July 31, the U.S. Treasury released its most recent Quarterly Refunding Announcement which revealed its financing strategy, presenting both positive and restrictive elements for global liquidity.

Decrease in Expected TGA Balance and Borrowing Needs

A significant highlight from the Treasury’s announcement is the revised projection for the Treasury General Account (TGA) balance by the end of Q4 2024. The Treasury now expects the TGA balance to be $700 billion, a decrease of $150 billion from the previous projection. Additionally, the Treasury has adjusted its borrowing needs for the fourth quarter, reducing it by $106 billion, now projecting a borrowing requirement of $740 billion. This follows its expectation for easing inflationary and growth pressures over the short-term.

These reductions in borrowing needs and the lower TGA balance are seen as positive for market liquidity, as they reduce the cash the Treasury pulls from the financial system, supporting broader economic stability.

Treasury’s Future Issuance Strategy

Despite the current focus on managing immediate borrowing needs, the Treasury also signaled its long-term strategy to shift towards issuing more longer-dated securities. The Treasury’s analysis suggests that while Treasury Bills (T-bills) are effective at absorbing unexpected increases in the federal deficit, the preference is to gradually issue more longer-term securities.

It remains to be seen whether this strategy will be successful. We would not be surprised to see the Treasury continually surprised by the larger than expected federal deficit, and as a result see it rely on a larger proportion of shorter dated t bills. As we have mentioned in previous webinars and market updates, the level of fiscal debt and the high interest rates, have combined to create a “reflexive cycle” in which the interest on the national debt is becoming a larger and larger portion of the deficit. While a recession would certainly cool things off, this doesn’t seem to be in the cards near term, at least, given the resilience we have seen in the consumer to borrow and spend.

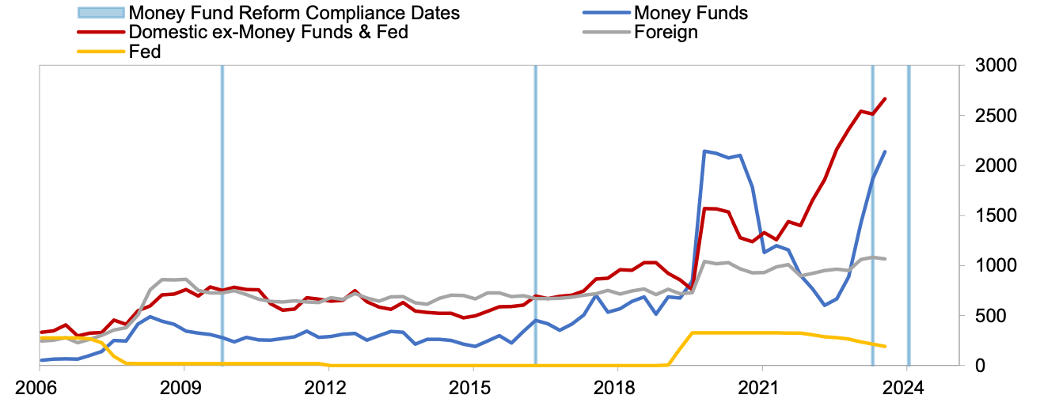

In addition, the Treasury is increasingly depending on domestic private borrowers to purchase T-bills. If this trend continues, the private sector may demand higher returns, further increasing borrowing costs.

Figure 1. Major Holders of T-bills ($billion)

Source: Federal Reserve Z.1, SEC, Federal Register

This strategic shift could lead to combined parallel shift upward and a steepening of the yield curve, where long-term yields rise relative to short-term yields. In our view, the Fed is much more likely to adopt a higher target for inflation than to derail the economy though tighter monetary policy. Despite our view, either scenario is possible so investors should stay diversified, nimble and ready to react.

Broader Economic Implications

As the federal deficit continues to surprise to the upside, the Treasury may increasingly rely on issuing shorter bonds rather than longer-term securities. If shorter bonds become a larger portion of the outstanding debt than expected, this could press inflationary pressures. This is because the Federal Reserve exerts more influence over the short end of the yield curve through its monetary policy actions, while the longer end is more driven by market-based inflation expectations. Further, the Fed is likely to favor a higher inflation target rather than tighter monetary policy. It desperately wants to cut rates this year, signaling just this week for a rate cut in September.

Strategic Investment Considerations

In this environment, investors should consider positioning their portfolios towards assets that are likely to perform well under inflationary conditions. Value stocks, which tend to be less sensitive to rising interest rates, alongside commodities and precious metals, offer potential protection against inflation.

Conclusion

The recent Treasury Quarterly Refunding Announcement offers a complex mix of factors for investors to consider. While the decrease in expected borrowing and the lower TGA balance are positive for liquidity, the potential increase in longer-dated securities over the short-term poses risks of tighter financial conditions. Investors should stay vigilant and consider diversifying their portfolios to mitigate potential risks.